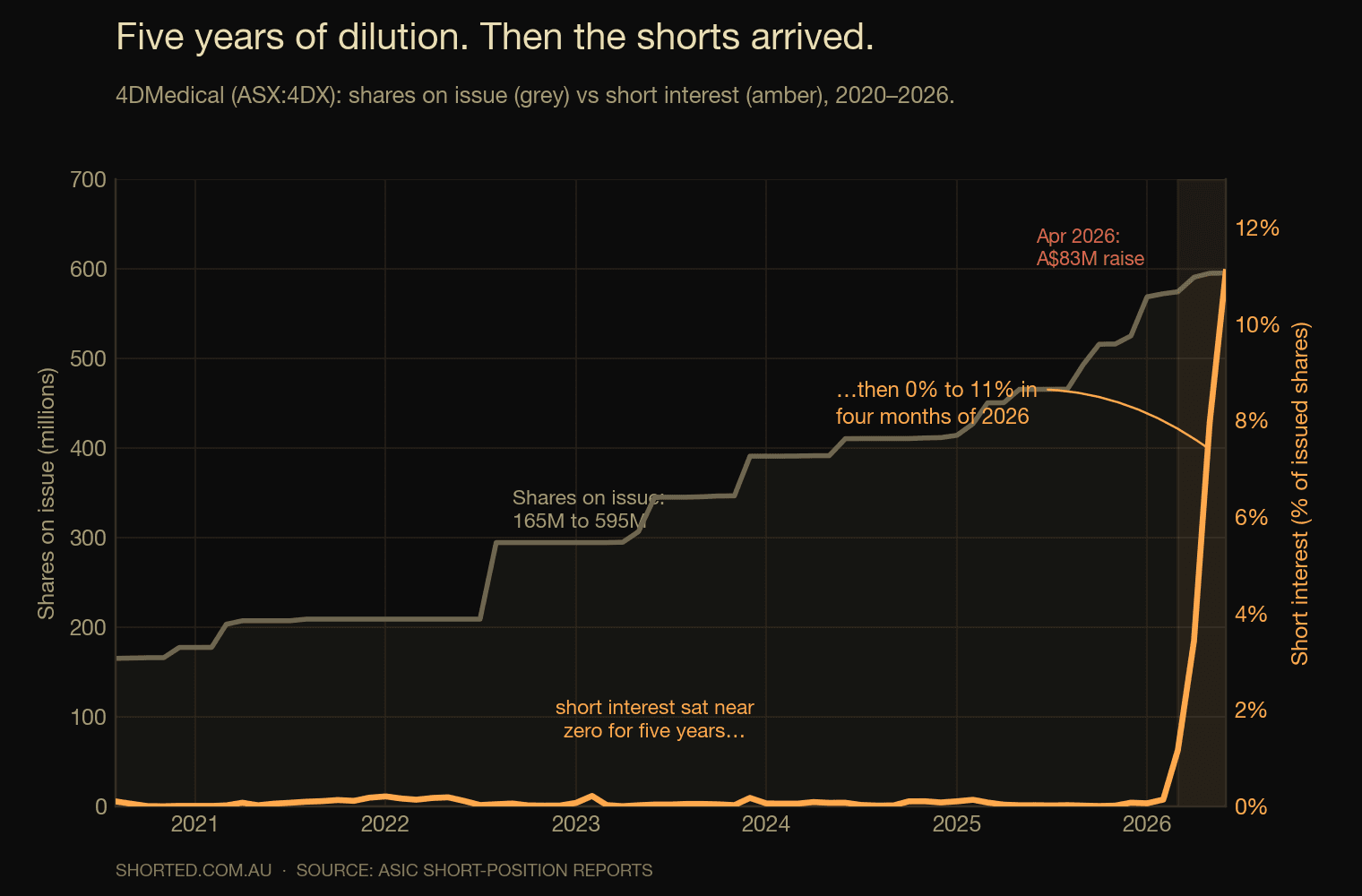

For five years, almost nobody bet against 4DMedical. The Melbourne lung-imaging group listed in 2020, issued shares at every turn, and watched its register swell from 165 million shares to nearly 600 million — and through all of it, the proportion of those shares sold short rounded to zero. Then, in the space of four months, short interest went from nothing to a record 11.3%, the second-highest of any medical-technology stock on the ASX. The shorts did not arrive because the science broke. They arrived because the share price stopped making sense.

The five-year nobody

4DMedical builds something genuinely novel. Its XV Technology turns an ordinary fluoroscopy or CT scan into a moving, quantitative map of how air actually moves through the lungs — regional lung function, not just anatomy — and in May 2020 its XV LVAS became the first product the US FDA cleared to dynamically quantify ventilation 1. The problem, for most of the company's listed life, was the gap between the elegance of the technology and the size of the business beneath it.

To fund that gap, 4DMedical did what pre-revenue medtechs do: it raised, and raised again. Each placement added paper, and the share count climbed in a near-unbroken staircase. Yet short sellers stayed away entirely — not because dilution is harmless, but because there was no rich valuation to bet against. You cannot short a stock for being expensive when it trades at a few hundred million dollars and almost everyone has forgotten it exists.

The twenty-four-bagger

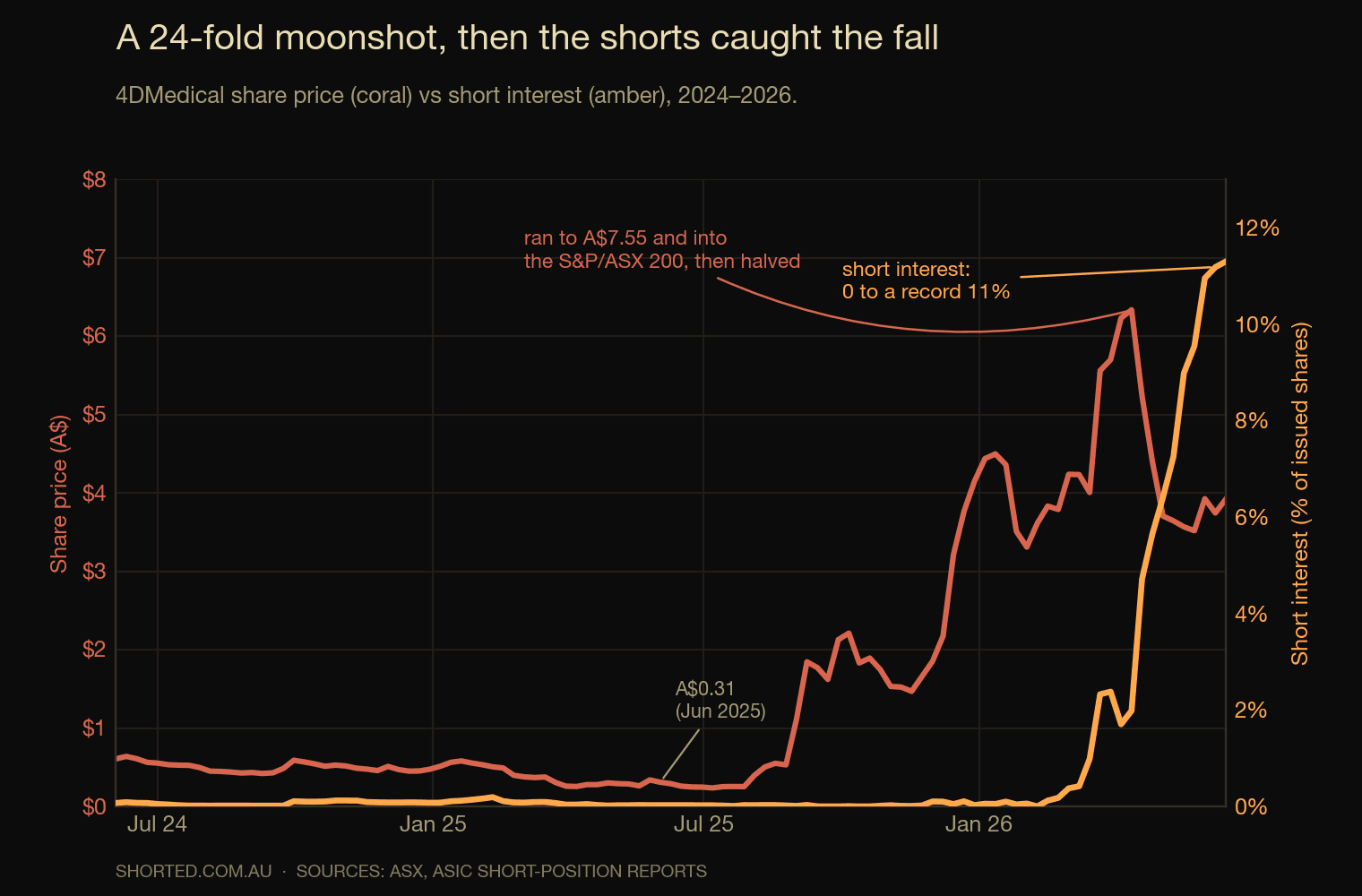

Then the story caught fire. In September 2025 the FDA cleared CT:VQ, which 4DMedical bills as the first and only non-contrast, CT-based ventilation–perfusion scan — a potential replacement for the nuclear medicine V/Q study 2. A European CE Mark followed in March 2026 3, US Medicare set a reimbursement path 4, and in April the company was admitted to the S&P/ASX 200 7. The share price, 31 cents in the middle of 2025, ran to A$7.55 by April 2026 — a twenty-four-fold move that turned a forgotten small-cap into a A$2.7 billion index constituent.

The fundamentals were, and are, improving fast. Scan volumes more than doubled to 151,905 in the December 2025 half, the installed base grew to 430 sites, and the software carries gross margins north of 90% R9. The company funded its ambitions from a position of strength, pulling in roughly A$233 million across two placements — about A$150 million in January at A$3.80 a share and A$83 million in March at A$5.90 56 — to finish the March quarter with some A$283 million in the bank 11. On the technology, the bulls have a real case.

Then the shorts arrived

What the bulls did not have was a price that left any room for error. At its peak 4DMedical changed hands at roughly 600 times its trailing revenue of about A$5.8 million, on a A$30 million annual loss R810. A multiple like that does not value a company on what it earns; it values it on a future in which almost everything goes right — every clearance converts to volume, every trial to a contract, every scan to a recurring fee — for years without a stumble.

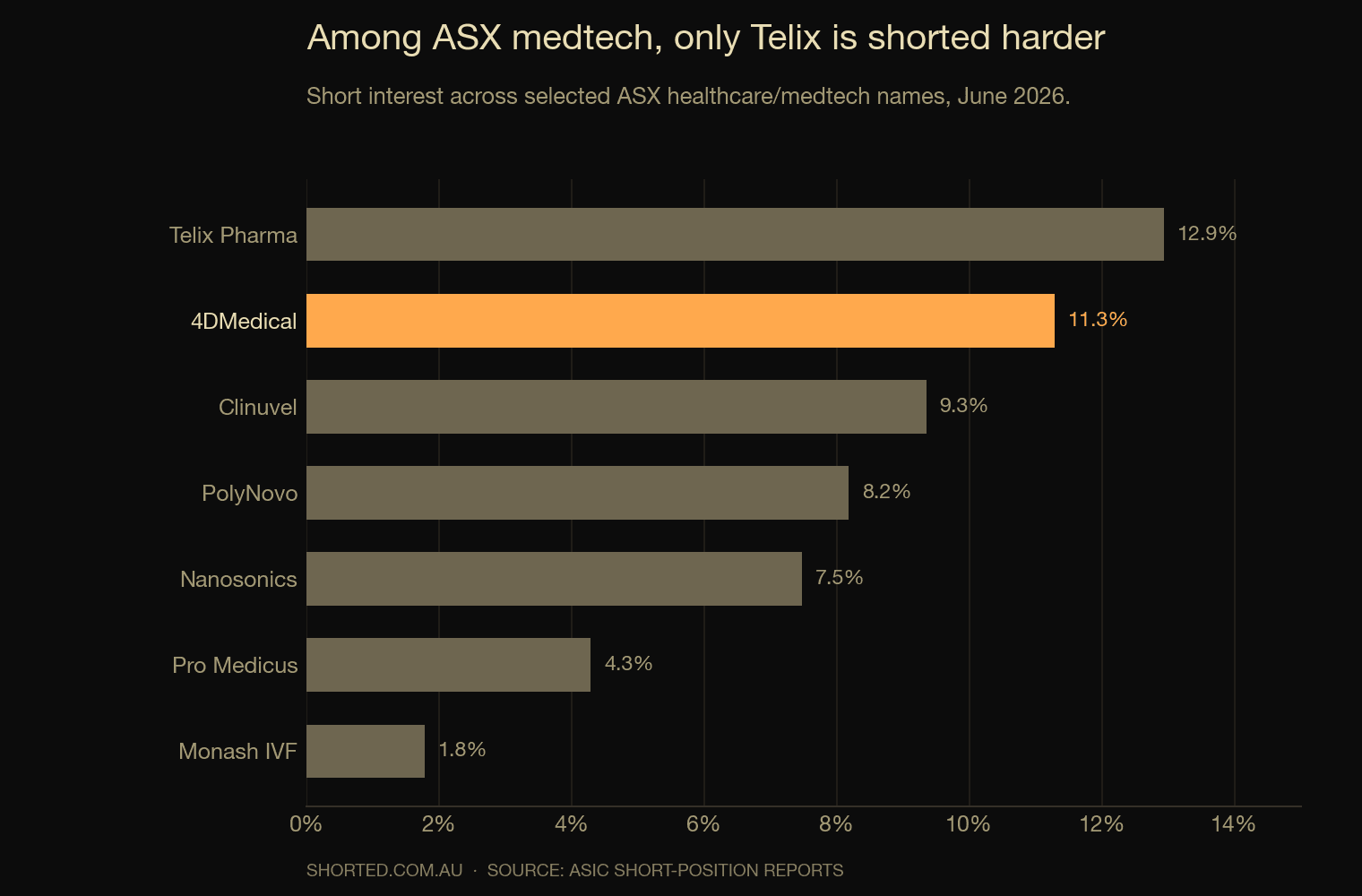

That is the gap short sellers stepped into. As the stock rolled over from A$7.55, short interest built fastest on the way down: from near-zero in February to 3.4% in April, 8% in May and a record 11.3% by mid-June. It is a remarkable signature — the bears were almost entirely absent through the run, then piled in to catch the air coming out. By June, only Telix Pharmaceuticals carried a heavier short load across the ASX's healthcare names.

The bear thesis is not that 4DMedical is a fraud or that XV does not work — the regulators and the scan counts say otherwise. It is narrower and harder to dislodge: that a company earning A$6 million cannot, for a while, be worth A$2.7 billion, and that serial discounted raises into a euphoric register tend to mark the moment the music slows. The shorts are not betting against the lungs. They are betting against the multiple.

The A$2.7 billion question

There is real danger in this trade for the bears, too. A genuinely disruptive imaging platform with 90%-plus margins and accelerating volumes is exactly the kind of stock that can sprint back up on a single contract, a Medicare code, or a takeover approach — and a record short position is dry powder for precisely that kind of squeeze. Analysts' intrinsic-value estimates run from single-digit cents to above A$11, which is another way of saying nobody really knows 10.

That is the tension a record short interest is pricing. On one side, a first-of-its-kind technology with the regulatory wins and growth to match; on the other, a valuation that ran four years ahead of the revenue and a register stuffed with freshly issued paper. The shorts spent five years ignoring 4DMedical and arrived, all at once, the moment the gap between the story and the numbers grew too wide to ignore. Whether they are early or wrong is now the most expensive question on the ASX's medtech bench.