Every crash has its villain, and for four centuries the villain has worn the same face. When shares in the Dutch East India Company buckled in 1609, the merchant Isaac Le Maire was accused of organising the first bear raid; Amsterdam answered with the world's first short-selling ban in 1610 1. When Wall Street collapsed in 1929, the Senate dragged the "bears" before the Pecora hearings and a furious President Hoover leaned on the New York Stock Exchange to stop them 2. America then spent seventy years with an "uptick rule" restraining short sales — written after the 1937 break and quietly repealed in 2007, months before the subprime crisis 3. When Lehman Brothers fell in September 2008, regulators on three continents reached for the same lever within days of each other 6.

Australia pulled it harder than almost anyone. On 22 September 2008, ASIC banned short selling outright — not just in the banks, but in every listed stock 4. The ban on ordinary shares lasted weeks; the one on financials ran into 2009. And out of that panic came the disclosure regime that makes this article possible: since 2010, every short position on the ASX has had to be reported and published 5. The dataset we are about to read is itself a monument to the reflex of blaming the shorts.

So it is worth asking what the shorts actually did — not in theory, but in the data. We pulled every reported short position on the Australian market since June 2010, roughly 2.2 million daily records, and lined them up against the market's worst falls. The crash-driving short seller, it turns out, is mostly a myth.

When the panic came, the shorts had gone quiet

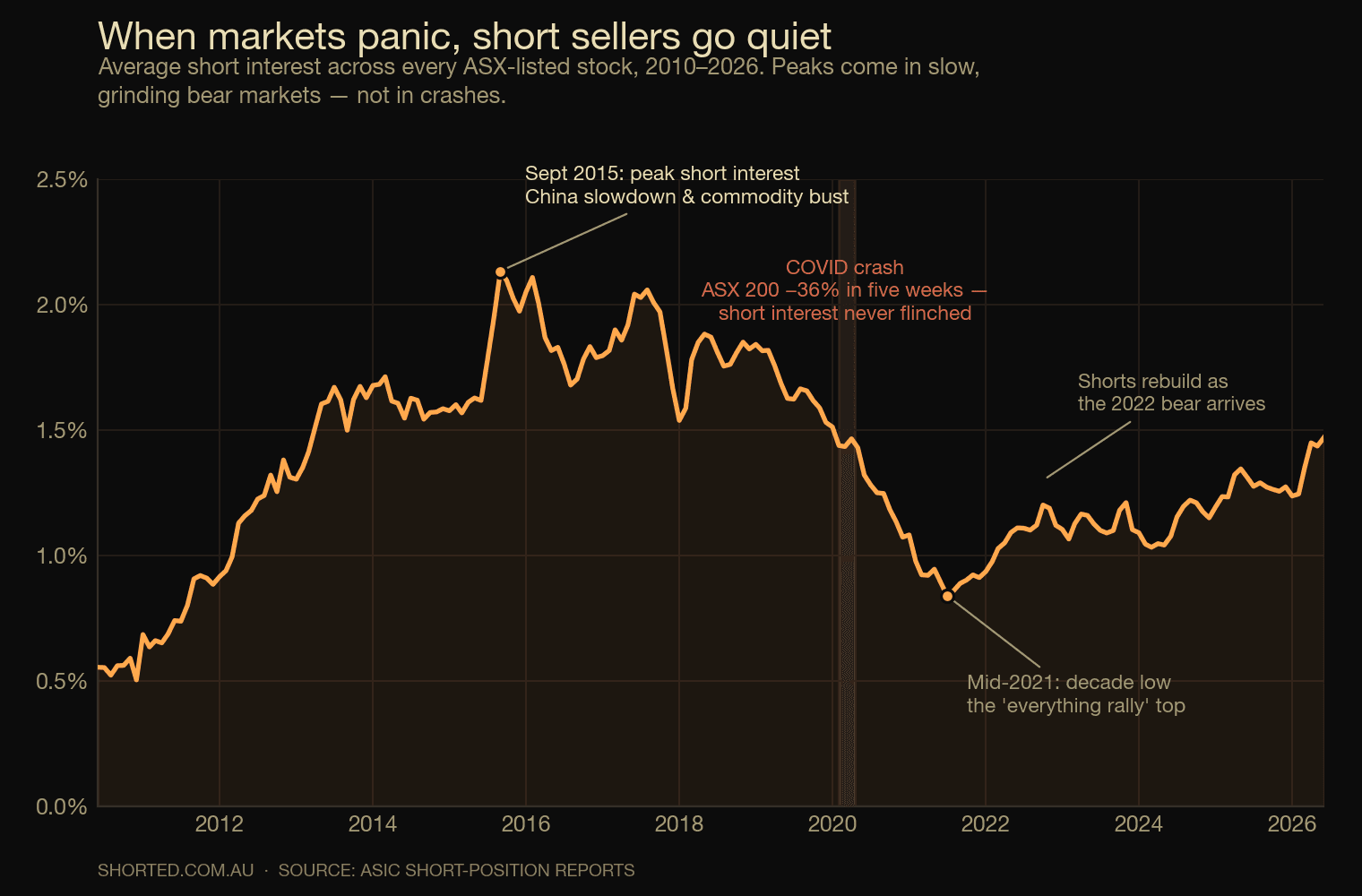

Average short interest across every ASX-listed stock has a shape, and the shape is the opposite of the one the villain story predicts.

The peak is not a crash. The most heavily shorted the Australian market has ever been was September 2015 — short interest touching 2.1% of shares on issue — during the slow, grinding sell-off in iron ore and the banks, with no single day of panic to point at. The next peak was late 2018, another grind. Short sellers do their best work in markets that are quietly deteriorating, not collapsing.

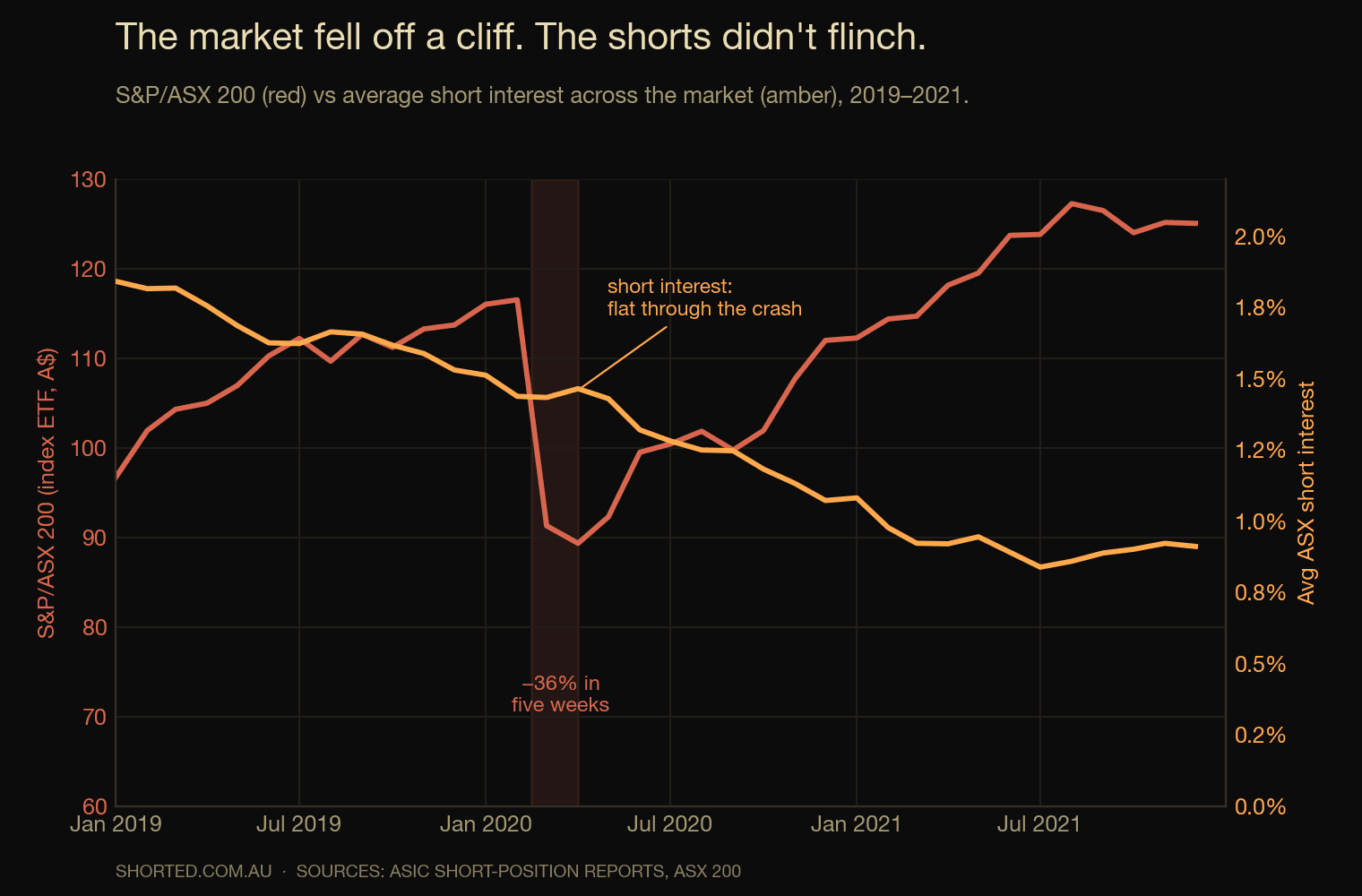

Then came the fastest collapse in the market's history. Between 20 February and 23 March 2020, the S&P/ASX 200 fell by more than a third 7 — five weeks that handed Australia its deepest economic contraction since the Second World War, a 7% fall in output in a single quarter 8. And short interest? It did not move.

Through the entire crash the market-wide average held between 1.4% and 1.5%, precisely where it had sat in January. If anything it drifted lower — and it kept falling, all the way to 0.84% by mid-2021, the least-shorted the ASX has been in the whole record, reached at the giddy top of the post-stimulus everything-rally. Short sellers were most absent at the exact moment a sceptic would have been most useful.

None of this means the shorts vanished — it means they were selective. Flight Centre has been shorted through every downturn of the last fifteen years: 4.8% in the 2011 European debt scare, 11.3% in 2015, 16.2% at the 2022 lows, and 11.5% today. Travel is the market's perennial canary, and the canary never really leaves.

The great rotation — and the squeeze that followed

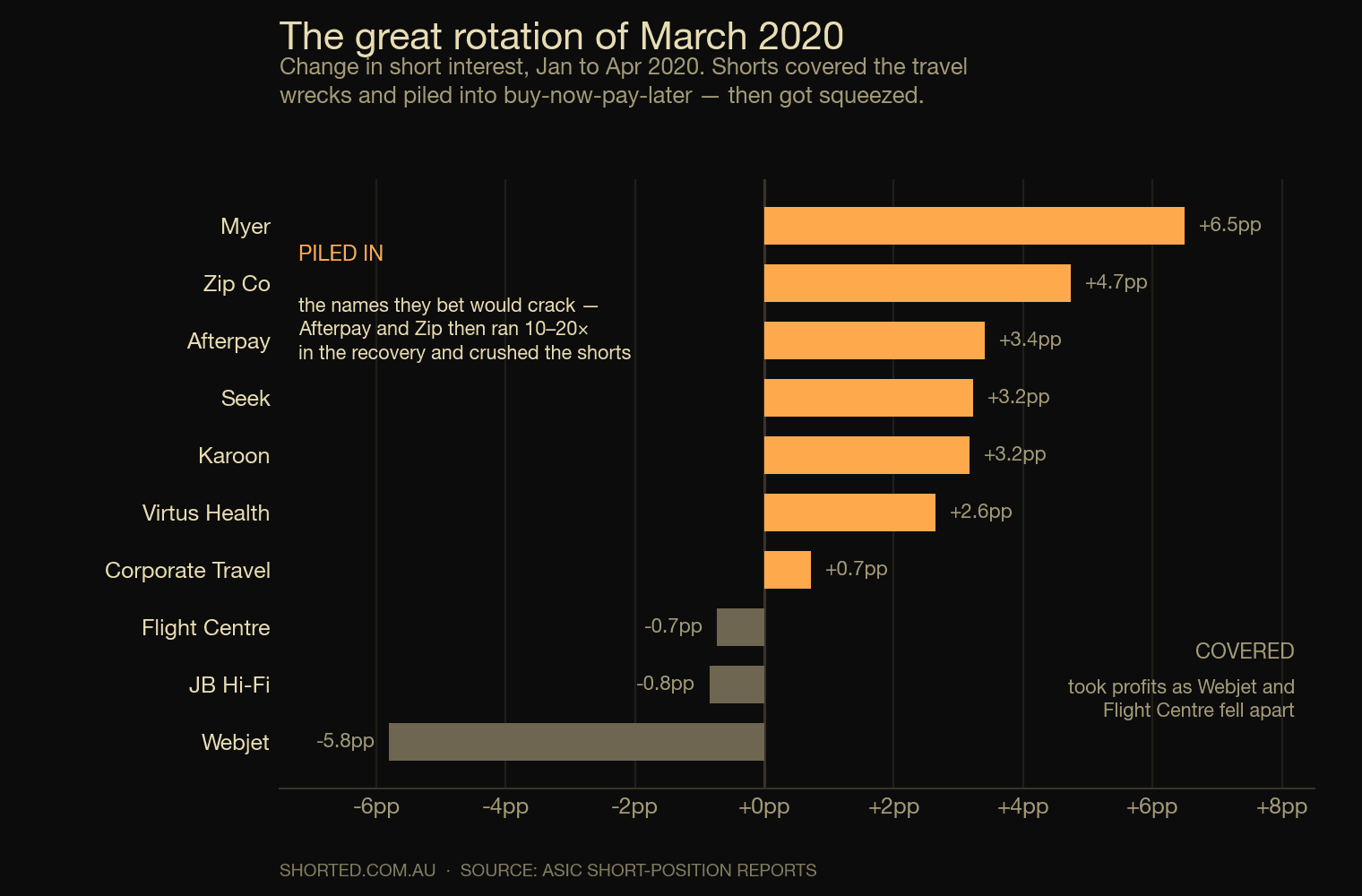

Behind the flat average, March 2020 hid a violent reshuffle.

The shorts who had ridden the travel and retail names down — Webjet, Flight Centre, JB Hi-Fi — quietly covered into the panic, banking the collapse they had predicted. Webjet's short interest fell from 10.1% to 4.3% in three months as the stock cratered; this is what an informed short looks like when it is right. At the same time, fresh money crowded into the names they thought would crack next: Myer, Seek, Karoon, and above all the buy-now-pay-later darlings, Afterpay and Zip, on a simple thesis — when the consumer breaks in lockdown, unsecured credit breaks first.

They were right about the recession and catastrophically wrong about the stocks. Afterpay bottomed near A$8 in the March rout and, carried by stimulus cheques and an online-spending boom, ran to roughly A$160 by February 2021 — a twenty-fold squeeze that ended with Block agreeing to buy the company in a deal first valued at about A$39 billion 9. Zip rose roughly tenfold off its low 10. The shorts had correctly forecast the worst economic shock in a generation and still been vaporised, because a falling market and a falling stock are not the same trade.

It is the oldest lesson in the book, and the famous blow-ups all rhyme. Porsche's hidden grip on Volkswagen in October 2008 briefly made VW the most valuable company on earth and cost short sellers an estimated €20–30 billion in days 11. The Reddit crowd torched Melvin Capital on GameStop in January 2021 12. A crash is not where shorts get paid; it is where the over-confident ones get carried out.

They had correctly forecast the worst economic shock in a generation and still been vaporised — because a falling market and a falling stock are not the same trade.

What the evidence actually says

If short sellers do not drive crashes, do the bans that follow each one at least help? The most comprehensive study of the 2008–09 episode — Beber and Pagano's survey of bans across thirty countries — found the opposite: bans drained liquidity, widened spreads, and slowed the market's ability to find the right price, without holding prices up 13. Examining the US ban alone, Boehmer, Jones and Zhang found shorting in the banned stocks fell by about 77% while their market quality deteriorated sharply — and their prices were no better for it 14. Across forty-six markets, the economists Bris, Goetzmann and Zhu found that where short selling is restricted, returns are more prone to severe negative shocks, not less 15.

The deeper finding is that short sellers carry information. Heavily shorted stocks reliably underperform — by more than a percentage point over the following month in the canonical study — because the people betting against them often know something 16. Abnormal short interest builds, on average, nineteen months before corporate fraud is made public 17. Jim Chanos was short Enron more than a year before it filed 18; short sellers flagged Wirecard years before its €1.9 billion hole swallowed it, and were rewarded with a German ban on shorting the stock and a criminal investigation — into them 19.

The canary, not the arsonist

The villain story survives because it is useful. A falling market needs a culprit who is not the board, the regulator, or the buyers who paid too much on the way up — and the short seller, secretive and profiting from decline, is purpose-built for the role. But the Australian data is unusually clean on the point, because the disclosure regime was born from exactly that suspicion and then recorded, day after day, what the suspects actually did.

What they did was stay home during the panic, get squeezed when they guessed, and do their real damage slowly, in the grinding markets where mispricings hide. They are the canary that goes quiet before the gas, not the spark that lit it. The next crash will arrive with its villain already named. A decade of data behind these charts suggests we are blaming the wrong bird.